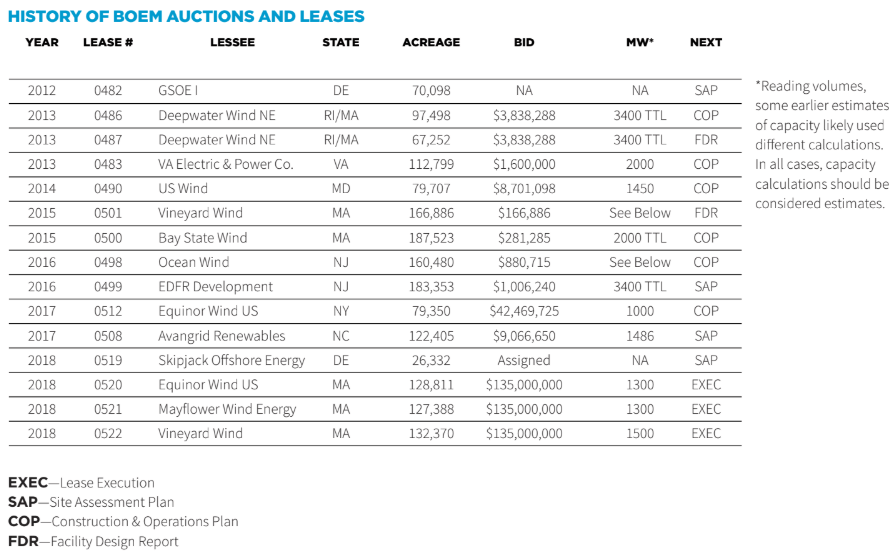

The U.S. Department of the Interior’s Bureau of Ocean and Energy Management (BOEM) to date has auctioned 16 U.S. offshore wind energy areas (WEAs) designated in federal waters for offshore wind development. Each area has been leased to a qualified offshore wind developer. The areas are located along the East Coast, from North Carolina to Massachusetts, and represent a total potential capacity of 21,000 MW of offshore wind power generation.

Market growth

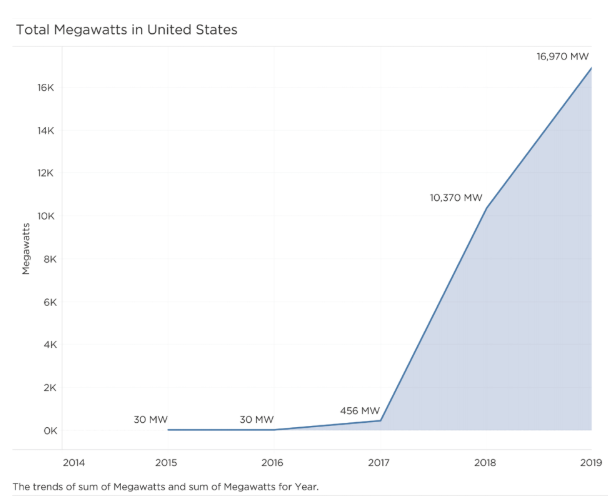

The U.S. offshore wind market currently stands at 16,970 MW, representing a subset of the total potential generation capacity. The market is defined as the amount of offshore wind electricity that could be produced by a state-supported financial mechanism. In the U.S., these financial mechanisms are usually either a power purchase agreement (PPA) or an offshore renewable energy credit (OREC).

In January, New York announced more than a three-fold increase in its commitment to support the development of offshore wind, from 2,400 MW to 9,000 MW. This jolted the U.S. market, with a 64% increase in market size.

More than $1 billion spent

Remarkably, nearly $1 billion was spent on U.S. offshore wind lease rights and projects in the last quarter of 2018. In October 2018, Ørsted acquired Deepwater Wind’s portfolio of lease rights and projects with government-backed financial mechanisms for $510 million. In December, three Massachusetts leases were won at a cost of $405 million, collectively. Equinor paid $135 million; Mayflower Wind, a joint venture of Shell and EDPR, paid $135 million, and Vineyard Wind, a joint venture of Copenhagen Infrastructure Partners and Avangrid Renewables, paid $135.1 million. This set a new record for U.S. offshore wind lease auctions.

Further, French utility giant EDF, in a joint venture with Shell, also bought US Wind’s lease rights in New Jersey for an undisclosed amount in the fourth quarter of 2018. The U.S. offshore wind sector is experiencing significant investments from major oil and gas companies and European utilities.

1,800 MW installed by 2023

To date, six commercial-scale projects and two demonstration projects comprise the U.S.’ offshore wind project pipeline, which totals close to 1,800 MW. These eight projects have received a state-supported financial mechanism – either a PPA or OREC. Developers emphasize that all eight projects will be constructed, installed and operating by 2023.

In May, New York will announce the winner of its first 800 MW request for proposals (RFP). In July, New Jersey will announce the winner(s) of its 1,100 MW competitive process. These two states will add 1,900 MW to the project pipeline, bringing the U.S.’ offshore wind project pipeline to almost 4,000 MW. Progress is expected to continue as Massachusetts intends to release its second RFP for at least 800 MW no later than June 30.

States drive market creation

Unlike the solar or onshore wind market, where corporate PPAs are fueling market growth, states are driving the creation and growth of the U.S. offshore wind market. Governors remain committed to the COP21 Paris Climate Agreement and view offshore wind as a clean energy utility-scale solution that can address climate change goals while simultaneously rapidly driving economic development. Recent climate change studies have added a new sense of urgency to the need for rapid transition to clean energy solutions.

States that have committed to the development of 16,852 MW of offshore wind by 2035 seem to have two common main policy drivers: increasing their renewable portfolio standards (RPS) and establishing offshore wind carve-outs. According to Lawrence Berkeley National Laboratory’s U.S. Renewables Portfolio Standards Annual Status Report, approximately half of all growth in U.S. renewable electricity generation and capacity since 2000 is associated with state RPS mandates.

Within the Northeast, Mid-Atlantic and West, all the regions driving the U.S. offshore wind market have RPS policies that continue to play a central role in supporting renewable energy growth.

In 2018, California, Connecticut, Massachusetts and New Jersey significantly raised their RPS goals. In addition, New Jersey and New York added new or increased offshore wind carve-outs. Last year, California also made a careful and deliberate transition with the passage of S.B.100 by the state legislature, which set targets for the state – the world’s fifth-largest economy – to have 100% carbon-free electricity by 2045. In general, most states have met their interim RPS targets in recent years, with only a few exceptions, reflecting unique, state-specific policy designs.

Conclusion

The U.S. offshore wind market is dynamic, and the outlook has never been better. The U.S. is moving forward and seizing the opportunities provided by state polices to create an offshore wind energy marketplace.

With each large-scale procurement and commitment, the industry gains greater momentum. There is no looking back or slowing down – only rapid growth, with developers and supply-chain companies making more investments, local residents being trained and ports bustling with new activity.

In 2020, BOEM is scheduled to auction the New York Bight’s four new wind energy areas, which will add a further 9,000 MW of offshore wind generation. When these areas are leased, it will bring the total U.S. capacity to 30,000 MW.

According to the International Renewable Energy Agency, the world demand for offshore wind will increase by 500,000 MW over the next three decades, and the U.S. is on track to contribute one-fifth of the world’s market. Offshore wind is becoming fully embraced as a growing U.S. economic engine and a critical part in the U.S. energy mix. It is the next big industry with big opportunities.

Liz Burdock is president and CEO of the Business Network for Offshore Wind. She can be reached at liz@offshorewindus.org.