Technology advancements are expected to continue to drive down the cost of wind energy, according to a survey of the world’s foremost wind power experts led by Lawrence Berkeley National Laboratory.

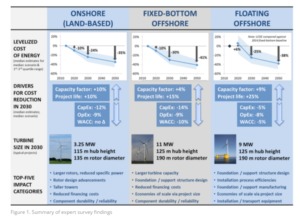

Specifically, these experts anticipate cost reductions of 24% to 30% by 2030 and 35% to 41% by 2050, under a median or “best guess” scenario, driven by bigger and more efficient turbines, lower capital and operating costs, and other advancements (see Figure 1).

These findings are described in an article in the journal Nature Energy.

The study was led by Ryan Wiser, a senior scientist at Berkeley Lab, and included contributions from other staff from Berkeley Lab, the National Renewable Energy Laboratory, the University of Massachusetts, and participants in the International Energy Agency (IEA) Wind Technology Collaboration Programme Task 26.

According to Berkeley Lab, the study summarizes a global survey of 163 wind energy experts to gain insight into the possible magnitude of future wind energy cost reductions, the sources of those reductions, and the enabling conditions needed to realize continued innovation and lower costs. Three wind applications were covered: onshore wind, fixed-bottom offshore wind and floating offshore wind.

“Wind energy costs have declined dramatically in recent years, leading to substantial growth in deployment. But, we wanted to know about the prospects for continued technology advancements and cost reductions,” said Wiser. “Our ‘expert elicitation’ survey complements other methods for evaluating cost-reduction potential by shedding light on how cost reductions might be realized and by clarifying the important uncertainties in these estimates.”

Significant opportunities for, but uncertainty in, cost reductions

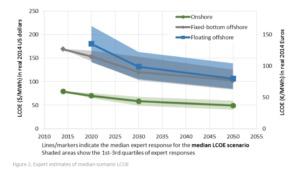

Under a “best guess” (or median) scenario, experts anticipate 24% to 30% reductions in the levelized cost of energy by 2030 and 35% to 41% reductions by 2050 across the three wind applications studied, relative to 2014 baseline values (Figure 1). In absolute terms, onshore wind is expected to remain less expensive than offshore, at least for typical projects, and fixed-bottom offshore wind is expected to be less expensive than floating wind plants (see Figure 2). However, there are greater absolute reductions (and more uncertainty) in the levelized cost of energy for offshore wind compared with onshore wind – and a narrowing gap between fixed-bottom and floating offshore wind.

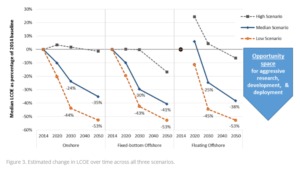

According to the study, there is substantial room for improvement, and costs could be even lower: Experts predict a 10% chance that reductions will be more than 40% by 2030 and more than 50% by 2050 (Figure 3, “low cost” scenario). Learning with market growth and aggressive research and development (R&D) are noted as two key factors that might lead to this low-cost scenario. At the same time, there is substantial uncertainty in these cost projections, illustrated by the range in expert views and by the high-cost scenario in which cost reductions are modest or non-existent.

Multiple drivers for cost reduction; larger turbines on the horizon

There are five key components that impact the cost of energy: upfront capital cost (CapEx), ongoing operating costs (OpEx), cost of financing (WACC), performance (capacity factor) and project design life. Recent years have seen significant reductions in the upfront cost of wind projects and increases in wind project performance, as measured by the capacity factor of wind facilities. Experts anticipate continued improvements in these two overall cost drivers, as well as reduced operating costs, longer project design lives and reductions in the cost of finance, with the relative impact of each driver dependent on the wind application in question (Figure 1).

A key change will be in the size of wind turbines, according to experts (Figure 1). For onshore wind, growth is expected not only in generator ratings (to 3.25 MW on average in 2030), but also in two factors that increase capacity factors: rotor diameters (135 meters in 2030) and hub heights (115 meters in 2030). Fixed-bottom offshore wind turbines are expected to get even bigger – to 11 MW on average in 2030 – helping to reduce upfront installed costs. A wide array of other advancement opportunities were also identified, with the top five impact categories for each wind application listed in Figure 1.

Comparison with other estimates of wind energy costs

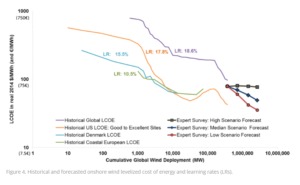

Expert views on the future overall levelized cost of onshore wind are consistent with the level of historically observed improvements (Figure 4).

However, a comparison of survey results with the broader wind forecasting literature shows that experts are, in general, more bullish on the prospects for further cost declines for onshore wind than the broader literature. One possible reason for this discrepancy is that the pre-existing literature for onshore wind sometimes focuses primarily on reductions in the upfront cost of wind projects, while expert survey results demonstrate that such improvements are only one means of achieving overall levelized cost of energy reductions. The existing literature may, therefore, understate the opportunity for further cost reductions for onshore wind.

“Onshore wind technology is fairly mature, but further advancements are on the horizon – and not only in reduced upfront costs,” said Wiser. “Experts anticipate a wide range of advancements that will increase project performance, extend project design lives and lower operational expenses. Offshore wind has even-greater opportunities for cost reduction, though there are larger uncertainties in the degree of that reduction.

“Though expert surveys are not without weaknesses, these results can inform policy discussions, R&D decisions and industry strategy development while improving the representation of wind energy in energy-sector and integrated-assessment models,” concluded Wiser.

The survey was conducted under the auspices of the IEA Wind Technology Collaboration Programme. Berkeley Lab’s contributions to this report were funded by the U.S. Department of Energy’s Office of Energy Efficiency and Renewable Energy.